{kind=link}

User needs driving the shift

Everyday Kenyan consumers want a simple, secure way to pay online and manage expenses without queuing at branches. That personal friction — time lost and paperwork — drives many to look for alternatives. For city professionals in Nairobi and beyond, solutions that issue a virtual card instantly matter; platforms such as didi finanzas promise exactly that, bundling virtual card issuance, basic KYC and immediate spending controls so you can start transacting within minutes.

What a virtual card actually offers

Virtual cards act like normal credit cards but exist only in software form: a card number, CVV and expiry tied to a digital wallet. They reduce exposure of your main account, enable one-time or merchant-specific payments, and work well with subscription services or online marketplaces. From a user standpoint, the key terms to know are tokenization and two-factor authentication — they make the card harder to copy and easier to revoke when needed.

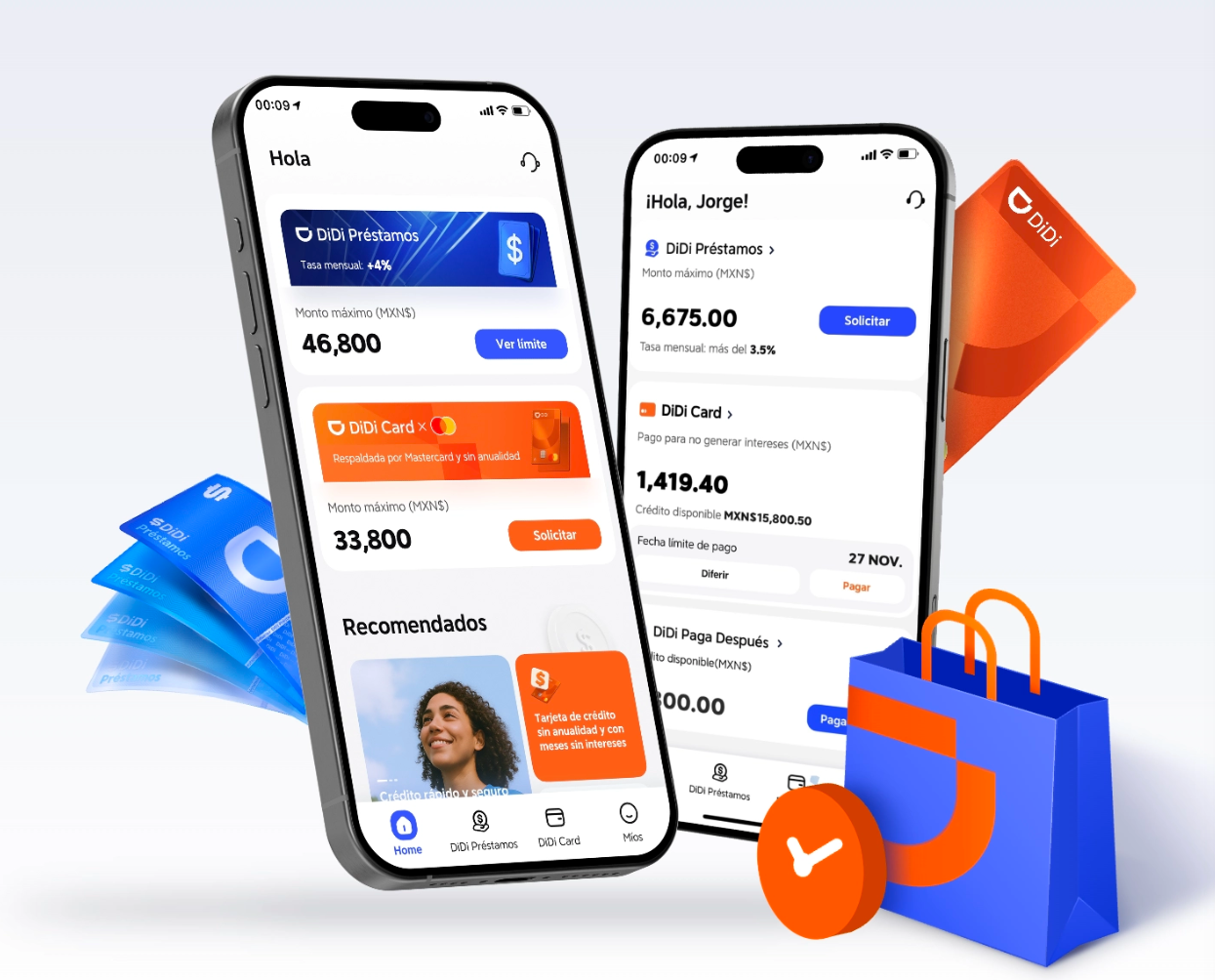

How DiDi Finanzas meets user expectations

DiDi Finanzas focuses on speed and control. Users can generate a virtual card through an app or web portal, set spending limits, and cancel cards instantly. For people balancing business and personal finances this is valuable: cards can be created per project or vendor, then closed when the job is done. The platform’s API-driven approach also helps integrate receipts and expense categories into accounting workflows for small enterprises.

Security, trust and real-world context

Kenya’s payments landscape is informed by M-Pesa’s influence since 2007; customers expect digital services that are resilient and transparent. On that note, many ask whether didi finanzas es confiable — trustworthy platforms typically demonstrate PCI DSS alignment, clear KYC procedures and visible privacy policies. Practical safeguards like tokenization, two-factor authentication and encrypted storage are baseline expectations for any provider handling payment credentials.

Common mistakes users make — and how to avoid them

People often treat virtual cards as a full substitute for financial discipline. Mistakes include creating too many cards without naming conventions, neglecting to reconcile transactions, and linking cards to accounts without reviewing access rights. Keep a concise naming scheme, export transaction feeds regularly, and limit card lifespans to the period you actually need them — these practices reduce risk and bookkeeping overhead.

Applying in three practical steps

Begin with verified ID and a link to a funding source; complete KYC within the app. Create a card with explicit limits and a merchant note if required. Finally, monitor activity via notifications and export statements to your accounting tool. For teams, set role-based permissions so only authorised staff create or cancel cards — a small governance step that prevents costly errors.

Comparing alternatives briefly

Traditional banks still offer perks like relationship lending and broader product suites. Prepaid virtual card services suit quick, low-friction spending. Payment gateways and fintechs offer robust developer APIs for automated reconciliation. Select based on whether your priority is convenience, integration or a wider financial relationship — each path has trade-offs worth mapping to your personal or business workflow.

Three golden rules for choosing a virtual-card solution

1) Security posture: Verify evidence of strong encryption, tokenization and two-factor authentication. 2) Operational fit: Ensure the provider supports the integrations you need (receipt export, API access, role-based permissions). 3) Local practicality: Check funding methods and customer support in-region — local responsiveness matters when a card needs quick cancellation.

Apply these metrics consistently and you’ll see measurable reductions in fraud exposure and reconciliation time. DiDi Finanzas fits this profile for many users because it balances instant issuance with control and local support — practical benefits that matter on the ground. —